The final 24 months have been a whirlwind for NFT lovers, with unprecedented demand for digital possession creating a brand new and thrilling asset class proper earlier than our eyes. However finally, all new toys lose their shine. And after a loopy interval of shopping for, promoting, and buying and selling NFTs, traders search new methods to leverage their belongings.

Enter the rise of fractionalized possession, staking, and NFT’s hottest new sector: lending.

You learn that proper. Individuals are lending their relatively-illiquid JPEGs for immediate payouts in crypto and money. And it’s develop into an enormous sector of the market.

It’s lastly time to interrupt down the fundamentals of NFT lending — the way it actually works, and the various kinds of lending fashions.

However first, a definition.

What’s NFT lending?

NFT lending is the act of collateralizing your NFT as a mortgage in alternate for instant crypto cost. And it solves the asset class’ most important drawback: liquidity. Relative to different asset courses, NFTs are comparatively illiquid — that means it’s not straightforward to rapidly promote your NFT for its designated market worth in money (or cryptocurrency). In different phrases, it may possibly take months for somebody to purchase your JPEG. Moreover, for traders with sizable funding allocations tied up in NFTs, fast entry to liquid capital can typically be a tall order. Loans additionally present NFT house owners with a way to generate non-taxable revenue, versus the tax implications of a sale.

Right here’s the way it works: The borrower wants a mortgage and places up an asset as collateral (NFT). The lender provides the mortgage in alternate for curiosity. But when the borrower can’t repay the mortgage on the agreed phrases, the lender will obtain the collateral. Most often, this course of is autonomously executed by sensible contracts on the blockchain.

However in all circumstances, NFT lending is executed through one in all 4 important fashions, every with its personal advantages and disadvantages.

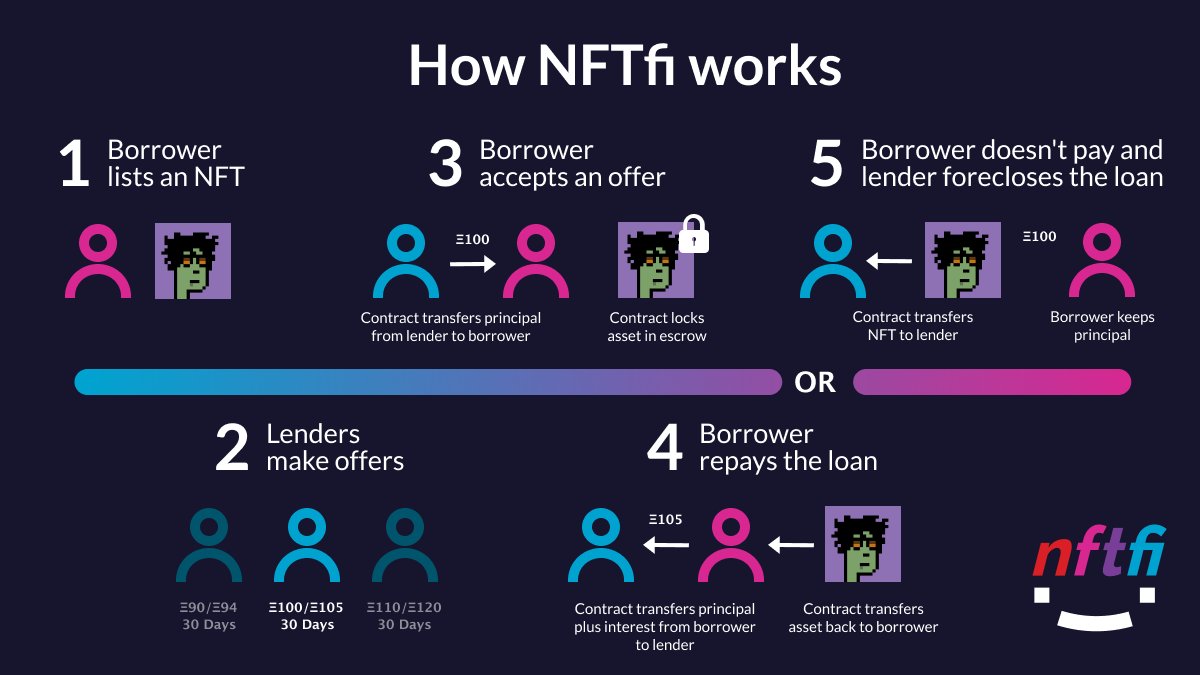

Peer-to-Peer: NFT lending platforms made easy

The best type of NFT lending is peer-to-peer, because it intently resembles the connection between a borrower and a lender you could find at your native financial institution.

Most transactions happen on peer-to-peer NFT lending platforms like NFTfi, and comply with an analogous course of. However not like borrowing in opposition to an asset with a steady worth, NFTs are a bit extra tough. The market is extremely risky, which implies the market worth of an NFT at this time could also be considerably totally different than its worth down the road. So how do you appraise its present worth?

The reality is, it relies upon. Most peer-to-peer lending platforms use a easy supply system to permit anybody to make loans and set phrases and not using a centralized or third-party middleman.

A consumer will record their NFT on the platform and obtain mortgage provides based mostly on the lender’s perceived collateral worth of the NFT. If the borrower accepts the supply, they’ll instantly obtain a wrapper ETH or DAI from the lender’s pockets. Concurrently, the platform will mechanically switch the borrower’s NFT right into a digital escrow vault (learn: sensible contract) till the mortgage is both repaid or expires. If the borrower defaults on the mortgage, the sensible contract mechanically transfers the NFT into the lender’s pockets.

Consolidating a number of NFTs with Arcade, and extra

Different platforms like Arcade enable customers to consolidate, or “wrap” a number of NFTs right into a single collateralized asset. Not like NFTfi, Arcade permits debtors to set their desired phrases and payback intervals upfront, after which hunt down a correct lender match by means of {the marketplace}. As soon as a match is found, the method begins.

The underside line? Peer-to-peer lending has emerged as probably the most favorable choice for each debtors and lenders, primarily as a consequence of its ease of use and safety. The pliability for each events to set phrases helps to account for uncommon NFT traits, and the sensible contract logic inside the escrow course of is pretty simple. Nonetheless, it’s essential to notice that peer-to-peer lending will not be the quickest mannequin, because it depends on a borrower discovering a lender keen to comply with set phrases mutually.

In keeping with Richard Chen, Normal Associate at cryptocurrency-focused funding agency 1confirmation, peer-to-peer lending isn’t solely the most secure mannequin, but in addition probably the most liquid and aggressive on the lending facet.

“In case you record a CryptoPunk on NFTfi, you’ll get a dozen provides fairly rapidly,” stated Chen in an interview with nft now. As DeFi yields have fallen, DeFi lenders have shifted towards NFT lending, since that’s the place the best yields in crypto are proper now.”

Peer-to-Pool NFT lending

Because the identify suggests, peer-to-pool lending permits customers to borrow instantly from a liquidity pool, reasonably than wait to discover a appropriate lender match. To assign worth to the collateralized NFTs, peer-to-pool platforms like BendDAO use blockchain bridges (Chainlink oracles, to be particular) to acquire ground worth info from OpenSea after which enable customers to immediately entry a set share of their NFTs ground worth as an NFT-backed mortgage. The NFT is then concurrently locked inside the protocol.

When liquidation occurs, it’s not based mostly on the time of compensation. As a substitute, it happens when the well being issue of the mortgage — which is a numeric illustration of security comprised of the collateralized market worth and the excellent mortgage quantity — falls beneath a sure threshold. Nonetheless, the borrower has 48 hours to repay the mortgage and reclaim their collateral.

In the meantime, lenders who provided liquidity to the liquidity pool obtain interest-bearing bendETH tokens, the place the value is pegged one-to-one with the preliminary deposit.

In brief, with peer-to-pool lending, you acquire pace however lose flexibility. Since these platforms assign worth based mostly on ground costs, house owners of uncommon NFTs are deprived, limiting the quantity of capital they will entry. The marketplace for borrowing can also be a lot smaller. Whereas platforms like Pine supply entry to extra NFT collections, BendDAO is just appropriate with choose blue-chip NFTs. However most crucially, there’s considerably better platform and hacking danger, in comparison with peer-to-peer, stated Chen.

“Given the illiquidity of NFTs, The worth oracles utilized in peer-to-pool will be manipulated rather more simply in comparison with different tokens,” stated Chen. To him, good NFT appraisal instruments like Deep NFT Value exist, however there’s “no oracle infrastructure but, so groups are working their very own centralized oracles that are susceptible to infrastructure hacking danger.”

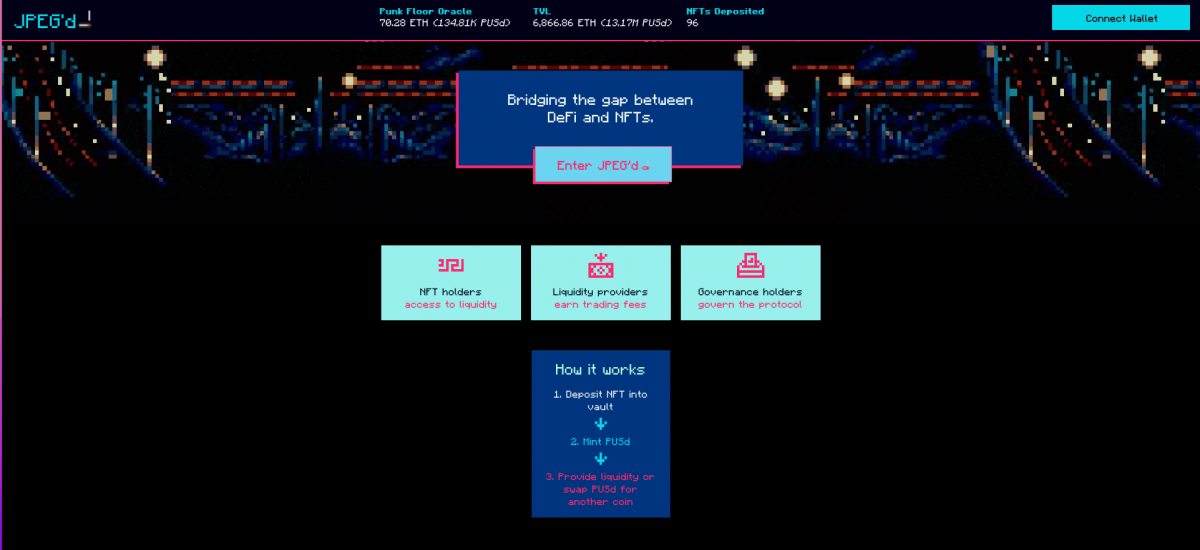

Non-fungible debt positions

A spin-off of MakerDAO’s collateralized debt position structure, the place debtors over-collateralize ETH (a dangerous asset) in alternate for DAI (a less-risky stablecoin), non-fungible debt positions supply an analogous deal. However on NFDP platforms like JPEG’d, as a substitute of depositing ETH in alternate for a DAI, debtors deposit choose blue-chip NFTs and obtain $PUSd, an artificial stablecoin pegged to USD, in return.

Like peer-to-pool lending, JPEG’d makes use of customized chainlink oracles to fetch and keep on-chain pricing information. The objective? To mix ground costs and gross sales information to cost collateral in real-time with excessive accuracy.

Non-fungible debt positions are nonetheless very new, and might want to mature extra earlier than it’s thought-about a good lending mannequin. Collateralized debt positions on MakerDAO are over-collateralized by 150 p.c (or 1.5 occasions), to mitigate the volatility of ETH. NFTs are much more risky, and the shortage of want for over-collateralization raises some concern in regards to the unpredictability of the NFT market and future liquidations. Moreover. JPEG’d is at the moment the one platform providing this construction, and is proscribed solely to CryptoPunks, so the accessible market is tiny, and the platform danger is sort of excessive. All issues thought-about, non-fungible debt positions ought to command shut scrutiny because it unfolds.

NFT leases and leasing through capital

Breaking rank with the opposite three buildings, NFT renting permits NFT holders to lease out their NFTs in alternate for upfront capital. Platforms like ReNFT function much like peer-to-peer marketplaces, enabling renters and tenants to transact with various rental phrases and agreements with out ready for permission.

Like exchanges on NFTfi, all rental transactions are facilitated by sensible contracts. However as a substitute of a borrower sacrificing an NFT as collateral and locking it right into a digital vault, the NFT is transferred to a different particular person’s pockets for a specified interval. In alternate, the “borrower” receives a lump sum of cryptocurrency. On the finish of the predetermined interval, the NFT is mechanically returned to its proprietor. That is the easy type of “lending,” since there aren’t any compensation phrases, curiosity, or fear of liquidation.

Not like different types of lending the place lenders are rewarded by incomes curiosity, NFT leases typically give lenders entry and credibility. The NFT area thrives on social proof, and proudly owning an costly NFT can enhance consideration and recognition within the area. Some communities are additionally token-gated, the place renting an NFT helps customers acquire publicity to individuals and experiences they might not in any other case purchase. Much like renting clothes, vehicles, or different objects of status-laden materials, the rising sector of NFT leases is poised to develop into one of the crucial enduring ones.

In the end, whether or not NFT lending is the correct choice for you particularly boils all the way down to your time horizon and danger tolerance. Like all crypto protocols, it’s important to do your personal analysis and never over-leverage or make investments cash you’re not comfy shedding.